See, here’s the thing most people scroll past: one US dollar now costs ₹94.33. Sounds like a traders-only problem – but it quietly shows up in your petrol bill, your cooking gas, and your next imported phone. So, let’s walk through what’s happening, and what India is doing about it.

Why a weak rupee matters and Why it’s slipping?

The exchange rate is just the price of a dollar in rupees. When it takes more rupees to buy one dollar, the rupee is “weaker,” and here’s why that hits you: India pays for its biggest imports in dollars – above all oil, nearly 90% of what we use. So, a weaker rupee makes that oil costlier in rupees, which flows straight into petrol, diesel, gas, and anything that’s moved or imported. As for why it’s slipping right now, it comes back to oil again: a conflict in West Asia earlier this year pushed oil to a four-year high, and since India imports almost all of it, we suddenly needed far more dollars for the same fuel. Add in nervous global investors pulling their money out, and the rupee slides – it hit a record ₹92 in March, and now it’s past ₹94. Oil has cooled since, but the pressure stuck around.

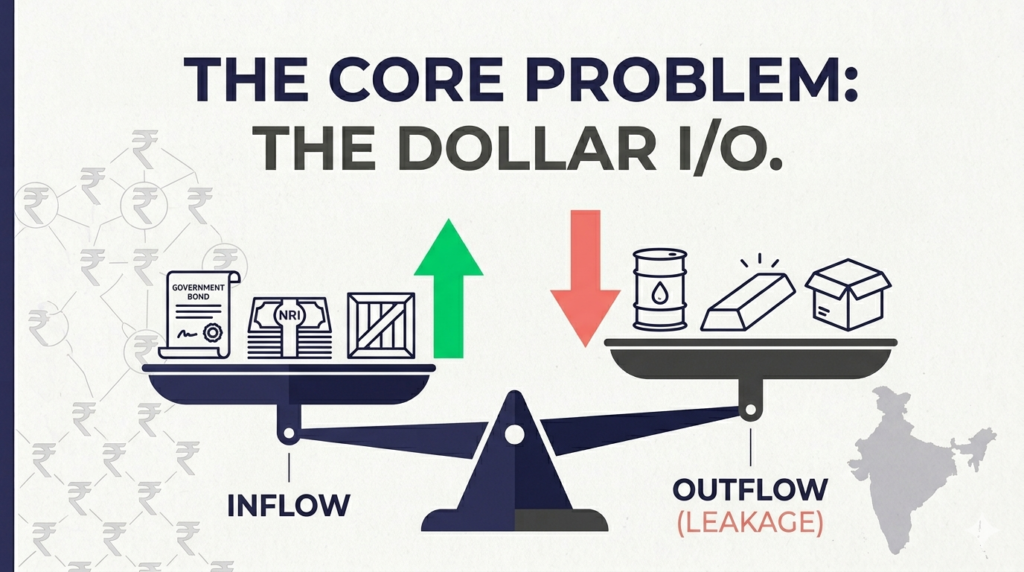

The core problem: India needs more dollars coming in – and fewer leaking out

Think of India like a household that earns in rupees but has a few big bills – mainly oil – that must be paid in dollars. To stay steady, it needs dollars flowing in, and it needs to slow the dollars leaking out. So, the government and RBI have been working both sides at once. Here are the main moves, each aimed at a different kind of money.

Door 1: Tax-free government bonds for foreigners

A government bond is just a loan you give the government, which pays you interest in return – one of the safest things you can hold. Foreigners used to get taxed on these earnings, so on June 5 the government scrapped that tax. The money showed up fast: over $2.2 billion in a single month, the most in over a year. Why it loops back to you? More buyers mean the government offers less interest to attract them, pulling its 10-year rate down to about 6.8%. And when the government’s rate falls, other rates (including your fixed-income returns) tend to drift down with it.

Door 2: Better NRI deposits – but only briefly

NRIs can park money in special accounts: NRE (in rupees) and FCNR(B) (in foreign currency, no exchange-rate worry). On June 17, the RBI lifted the cap on the interest banks can offer – for FCNR(B) of 3–5 years and NRE of 3 years and above – until September 30, 2026. One bank’s research team thinks it could pull in ₹5.2–6.2 lakh crore. Two things if you’re an NRI: moving money from an NRO to an NRE account doesn’t qualify, and the window shuts September 30.

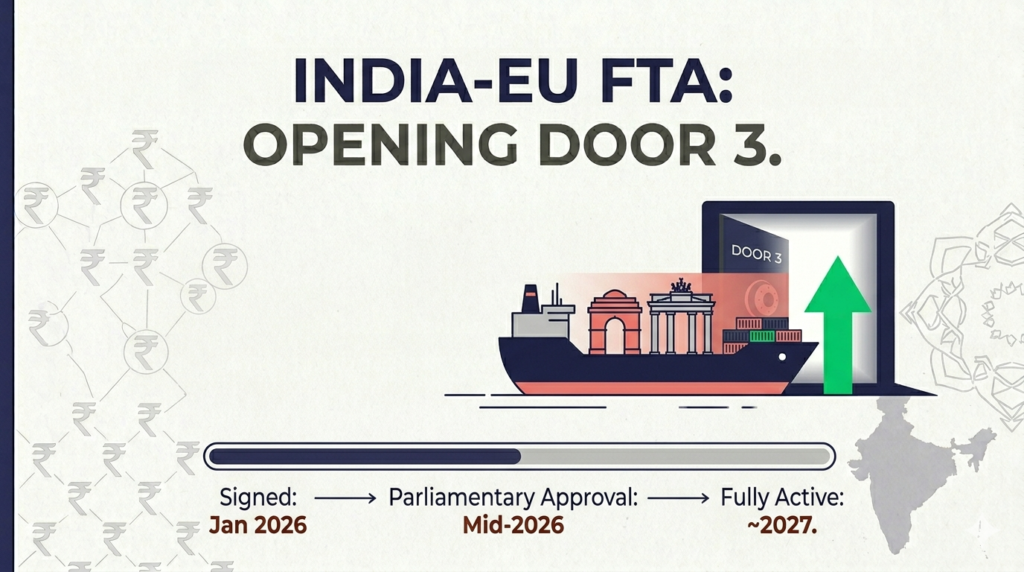

Door 3: A giant trade deal with Europe

A free trade agreement means two regions drop most of the taxes on each other’s goods so trade flows freely. On January 27, 2026, India and the EU signed one after nearly two decades of talks – India cutting duties on 96.6% of EU goods, the EU on 99.5% of India’s, over seven years, linking a market of two billion people. This is the slow-but-solid door: it builds long-term trade and credibility, not instant dollars. It still needs EU parliamentary approval (around mid-2026) and likely kicks in fully around 2027.

Door 4: They made imported gold and silver more expensive

Here’s a leak most people miss: Indians love gold, and almost all of it is imported, paid for in dollars. Buying had jumped in early 2026 (imports up to about 83 tonnes a month from 53 tonnes a year earlier), draining dollars just as the rupee struggled. So, in May, the Prime Minister asked Indians to pause gold buying for a year, and the duty on gold and silver was raised from 6% to 15% – costlier gold means less buying, so fewer dollars leave. Gold and silver are nearly 11% of India’s imports, so even a small dip saves serious dollars. The catch for you: gold just got pricier to buy.

Door 5: The push to cut the tax on your long-term gains

This one’s a debate, not a done deal. Hold shares or equity mutual funds over a year, and your gains above ₹1.25 lakh are taxed at 12.5% – that’s long-term capital gains (LTCG) tax. Investors are pushing to cut it to 10%, some even to scrap it on equities. The rupee connection: the more Indians stay invested in their own markets, the less India leans on flighty foreign money that can rush out overnight. Budget 2026 kept LTCG at 12.5%, but the finance minister has said she’s open to investors’ concerns, with proposals on the table. So, treat it as “maybe coming,” not done – but if it lands, it directly lifts your post-tax equity returns.

So, will it work?

Honestly – sensible, but it’s not magic, and each one has a catch. The bond money can leave as fast as it came if US rates look better. NRI deposits have disappointed before, since banks can raise money cheaper elsewhere. The trade deal has friction – Europe’s new carbon tax could squeeze Indian steel and aluminium. The gold duty can quietly push buyers toward smuggling and the grey market, which blunts the benefit. And the LTCG cut is still just a proposal – Budget 2026 didn’t touch it, so don’t bank on it. Call it a coordinated effort to steady the rupee, not a guaranteed fix.

What this means for you?

If you’re a saver or investor: high fixed returns may slowly ease as rates drift down, so it’s worth acting before they settle lower.

If you’re an NRI or have family abroad: a genuinely good but time-limited deposit window closes September 30 – mind the NRO-to-NRE catch.

If you’re planning to buy gold: it’s costlier now thanks to the higher duty, so factor that in.

If you’re in equities: keep half an eye on the LTCG debate, because a cut would lift your take-home returns.

And if you’re just a consumer: watch the rupee and oil together, because those two decide what you pay at the pump and the checkout more than anything else.

A weak rupee isn’t a disaster – it’s a signal. India’s working to steady it, and how well these moves hold up over the next few months will shape interest rates, prices, and the investment climate around you. Understanding why is the first step to making smarter calls with your money – which is exactly what we’re here to help you do.

For general educational purposes only; not investment advice. Figures based on publicly available information as of June 2026.